How Miden Brings the Power of Crypto Rails to Neobanks

A neobank’s job is to make money simple.

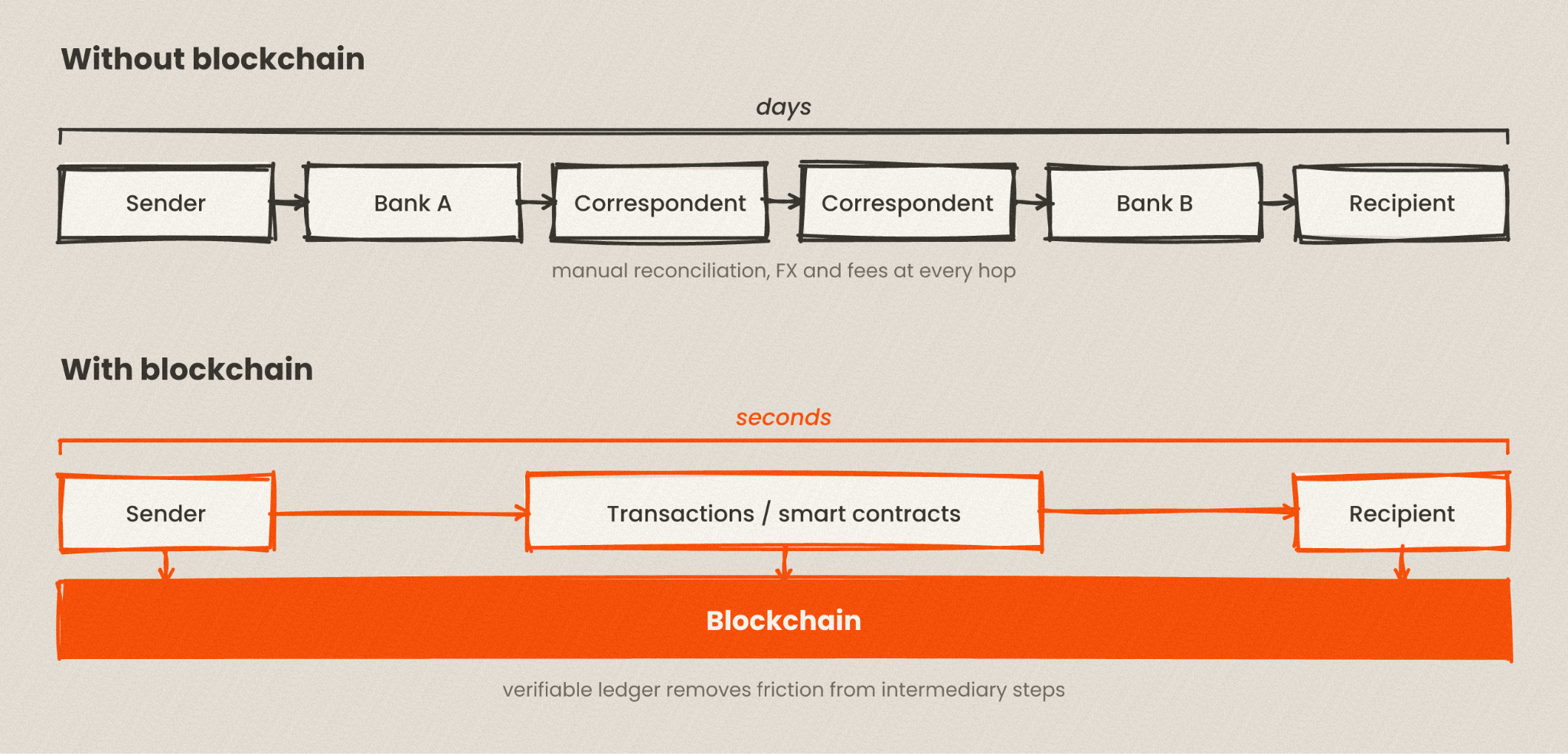

Under the hood, though, money is anything but simple. Cross-border money movements in particular still depend on a legacy patchwork of banks, payment processors, correspondent relationships, manual reconciliation… The list is long. Every new market, currency, or partner adds another moving part, and the fees that go with it.

Neobanks first emerged in the 2010s to make finance feel more like the modern internet: intuitive, digital-first, and easy to use. But the experience they offer is only as good as the financial infrastructure underneath it.

That is why blockchains are attractive infrastructure for consumer finance. They offer new tools and plumbing: programmable assets, portable value, global settlement… basically financial rails that can operate outside the limits of a single banking stack.

But, and it is a big “but”: traditional blockchains are transparent, and having financial data out there in the open is a total no-go for real-world applications.

Why neobanks need blockchains with private rails

Public rails may be useful for settlement and programmability, but public-by-default financial graphs are the wrong default for everyday money, consumer or business. A consumer app that makes balances, recipients, transfer timing, savings behavior, and any type of financial activity legible to the public internet is not likely to be attractive to anyone who cares about their financial privacy. Which is most of us.

AI makes that exposure even harder to ignore. Public transaction histories were already traceable; now they are easier to search, connect, and turn into behavioral patterns.

That’s why the world needs Miden, a blockchain that builds in privacy from the ground-up without sacrificing convenience, compliance, or capacity. Private rails only matter if they are usable, governable, and able to operate at real application scale.

On Miden, which goes to mainnet this summer, transactions are private-by-default. And because Miden does not need to publish all transaction data onchain, private transactions are cheaper to process than public transactions.

Miden is ideal infrastructure for neobanks. It keeps the benefits of blockchain rails while changing the privacy model that normally makes blockchains unusable for consumer finance.

How to build a neobank on Miden

Let’s look at how a consumer-facing neobank can be built on top of Miden.

Sempo is a soon-to-launch neobank serving the MENA region, where consumers often pay high fees for international payments and are sometimes frozen out of the mainstream financial system entirely. Based on USD-denominated stablecoin infrastructure, it facilitates peer-to-peer payments across borders without the headaches of traditional systems or an earlier era of crypto.

Sempo designed its product around a simple observation:

Crypto rails are powerful, but crypto UX is not.

Neobanks already abstract away the complexity of traditional finance; a blockchain-powered neobank has to do the same for wallets, signatures, transaction mechanics, and the underlying infrastructure.

The goal is simple: users open the app, understand what they have, send money, receive money, recover access, and trust that the product works in the background. The important thing is that it feels like a normal financial app, never like “using a blockchain.”

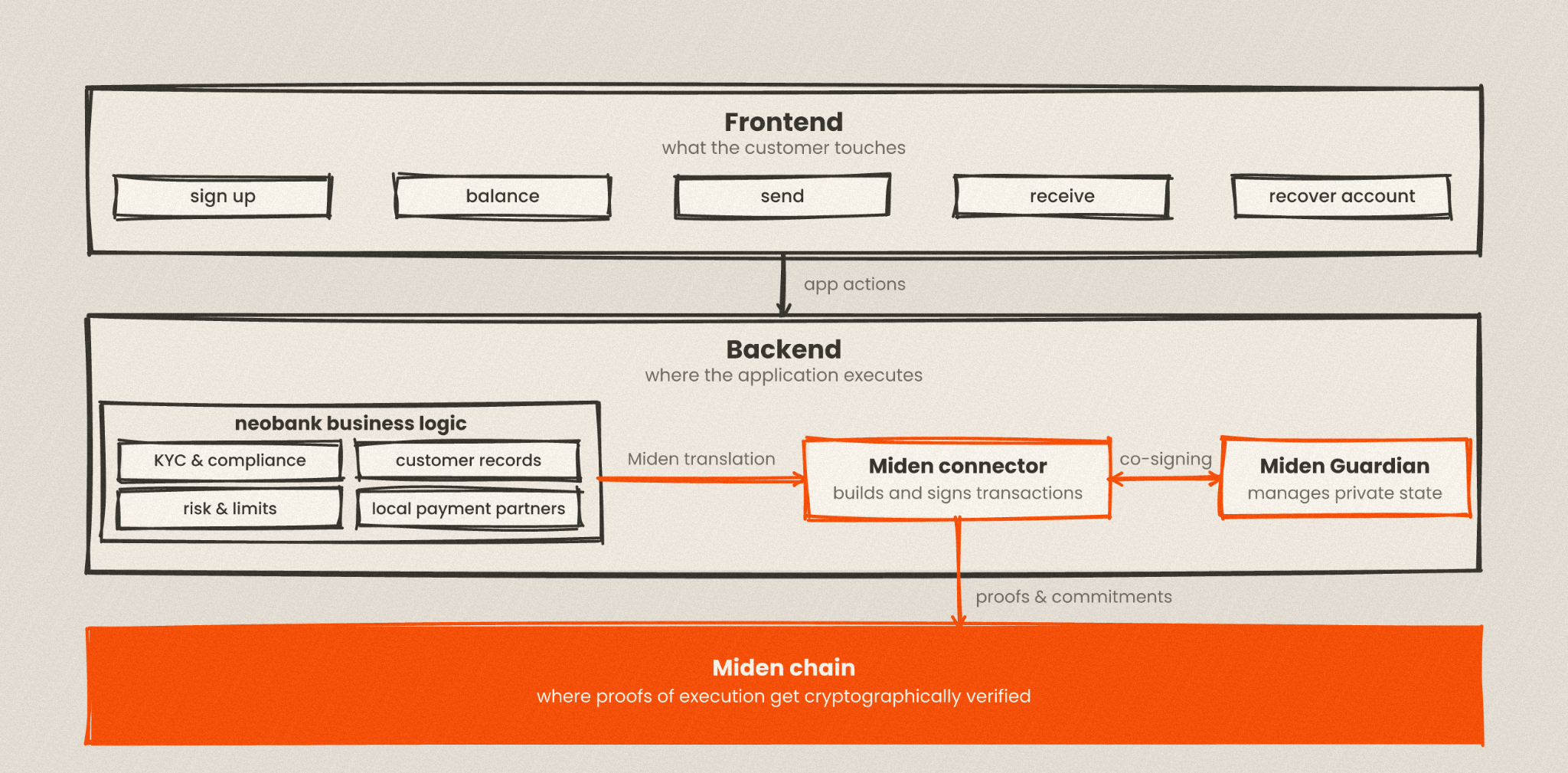

To achieve that, the architecture is designed around three layers with strict responsibilities: frontend, backend, and the chain.

The frontend is the app the customer touches: sign up, see their balance, send, receive, and recover their account.

The backend is where most of the neobank logic lives: it handles onboarding, compliance workflows, customer records, support, local payment integrations, risk rules, fees, limits, and the Miden connector. The connector is the part of the backend that turns normal app actions, like “create an account,” “show this balance,” or “send this amount,” into Miden operations.

The Miden chain sits underneath that backend. Its job is to verify proofs and certify that the ledger is correct, without forcing the customer’s financial data to become public.

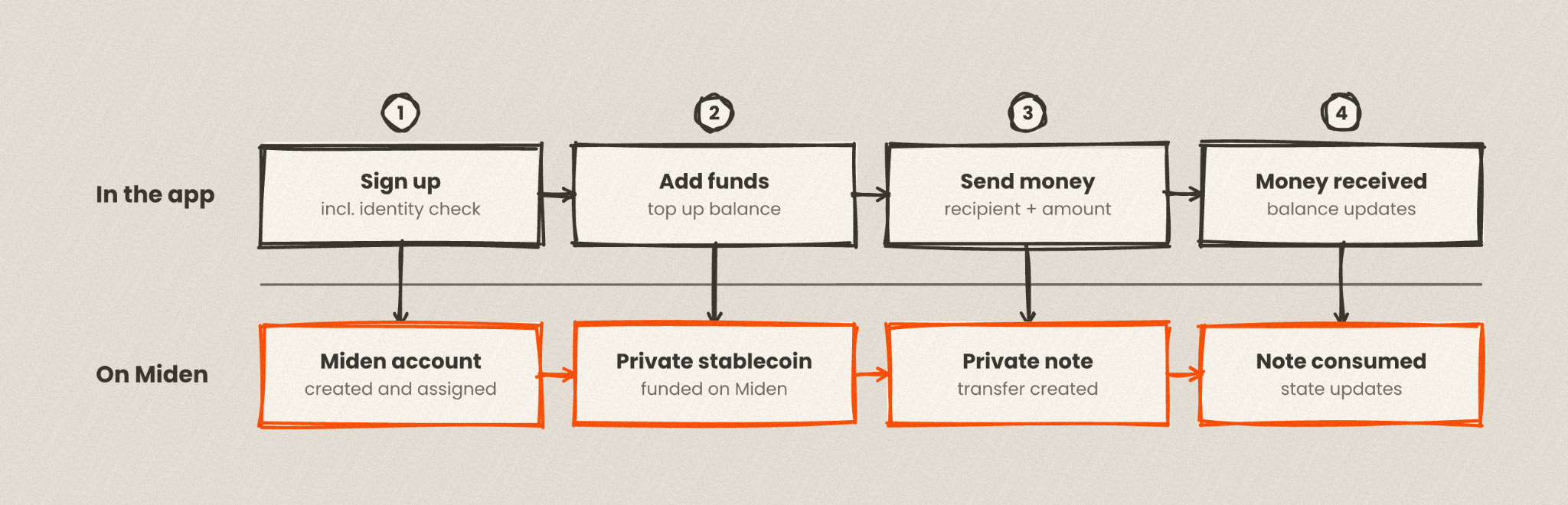

A simple transfer flow

Take a basic remittance flow where customers are sending money from, say, Egypt to Bahrain.

First, users sign up. The neobank handles the familiar part: identity checks, customer record creation, and whatever local requirements apply. Under the hood, the system creates or assigns a Miden account for that customer. In a real consumer app, this can be prepared in advance so onboarding feels instant rather than waiting on blockchain operations.

Second, users add or receive funds. The neobank can connect to local payment partners, bank rails, card networks, on-ramp/off-ramp providers, or stablecoin liquidity, depending on what fits their market. Miden does not replace those entry points. It becomes the private rail, powered by a private stablecoin, where the user’s programmable financial state is represented once value is inside the system.

Third, users send money. In the app, this feels like any other transfer: choose recipient, enter amount, confirm. Underneath, Miden can represent the transfer with private notes. The sender’s side creates the transfer; the recipient’s side receives it. The app can hide that lifecycle so the user sees a simple send/receive experience.

Fourth, the neobank reconciles what happened. This is where blockchain rails matter. Instead of every jurisdiction, partner, and internal system relying only on separate ledgers and manual reconciliation, the neobank can anchor flows to a shared verifiable ledger. Miden adds the missing privacy property: the network can verify valid state changes without turning customer activity into public financial data.

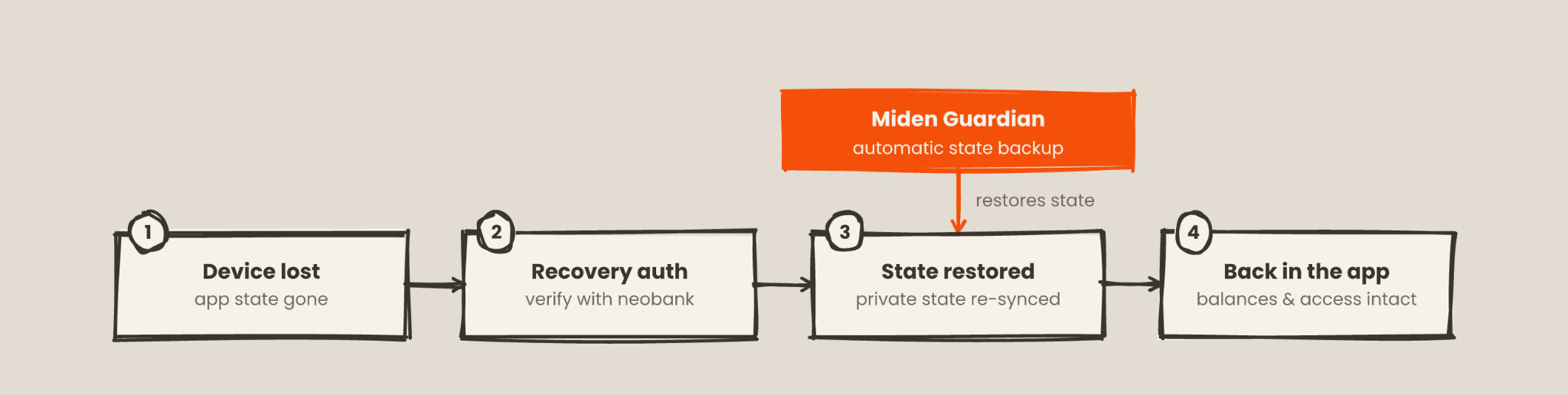

Recovery, continuity, and compliance

Separately, the user needs continuity. Phones can be lost, services can go down, and accounts need to be recoverable. A B2C neobank cannot tell users that private state is their problem: “Oh, if you lose your phone, you lose your money.”

It needs backup, restore, sync, and recovery flows that feel normal and easy. This is the role of Miden Guardian, a service run by the neobank itself, which helps with private account-state continuity by acting as an automatic, pre-transaction backup for user accounts. It can also be used to enforce policies defined by the user (such as monthly transaction volume caps or a whitelist of recipients), as well as compliance rules required by local regulations (typically around sanctions lists or AML screening).

The broader point: privacy works for consumer finance only if it is operationally usable, and that’s what Guardian enables.

Conclusion

Neobanks need infrastructure that can move across markets, connect partners, support programmable assets, and give operators a reliable way to reconcile what happened. Public blockchains are a great start, but they expose too much confidential information for real consumer finance.

Miden keeps the useful parts of blockchain infrastructure while giving neobanks the privacy model they need to build actual financial products for the real world.

Guardian strengthens that model by making private state easier to back up, restore, and govern. It also allows operators to comply with local laws and regulations. The result is simple for the customer, operationally usable for the neobank, and verifiable for all parties.

.jpg)

.jpg)